Does your team understand what’s really at stake when its risk management fails? Even a modest claim can have outsize consequences for your firm.

What’s the real cost of a claim to your design firm? Many people, including firm leaders, assume insurance is a safety net that catches everything. But the reality is that a claim, even a small one, can cost a firm hundreds of thousands of dollars.

One of the most valuable investments a design firm can make is increasing its staff’s risk awareness. This helps team members recognize those situations that don’t feel right and gives them the tools to speak up before a costly claim diverts the firm’s attention away from doing business. Your staff needs to know that even a relatively modest claim can carry major financial consequences. Suppose your firm faces a $100,000 lawsuit. If your professional liability (PL) policy has a $25,000 deductible, you’ll need to generate $250,000 in new revenue (assuming a modest 10% profit margin) just to recover the deductible amount.1

And that’s just the beginning. Consider the many hidden costs insurance doesn’t cover:

- Lost billable time. Principals may spend 200 hours or more working with legal counsel to defend a claim, including gathering documents for discovery, preparing for and participating in depositions, and communicating with counsel and experts. At $180 per hour, that’s $36,000 in unrecoverable billable time. Using the formula above, you’d need $286,000 in additional revenue to make up for the cost of the claim [$250,000 to cover the $25,000 deductible and $36,000 in unrecoverable billable time].

- Redesign costs. Agreeing to provide revised drawings in response to a claim usually increases the lost billable time incurred by the firm because that work is uncompensated and uninsured.

- Damaged relationships. A claim doesn’t just affect your firm’s bottom line. It can also affect your firm’s relationship with the client involved with the claim and the firm’s reputation with existing and future clients, even those not involved in the dispute.

- Team morale. Internally, claims can lead to stress, finger-pointing, and burnout, especially when employees feel blindsided by issues they didn’t realize were risky.

- Increased premiums and a higher deductible. Large claims can increase the cost of your insurance and lead to a higher deductible.

A tale of two projects: early action vs. escalation

The following contrasting examples illustrate the importance of recognizing and acting on potential problems:

Project A: A project manager noticed inconsistencies between the client’s oral instructions and the contract’s written scope. Rather than proceeding, she documented the discrepancy and requested clarification from the client. This led to a scope amendment that added $15,000 to the fee—and prevented what could have become a claim by identifying a discrepancy in the scope of services between the design firm and its subconsultant.

Project B: A junior engineer observed the contractor deviating from specifications but assumed the senior engineer was aware. Months later, performance issues emerged, and the client filed a claim against the design firm for inadequate construction observation. The result: a $50,000 deductible, $12,000 in lost principal time—and a fractured client relationship.

Both situations showed early warning signs, but only one was successfully resolved, because the designer took action.

From unbilled time to lost opportunities, the true cost of a claim is more than writing a check.

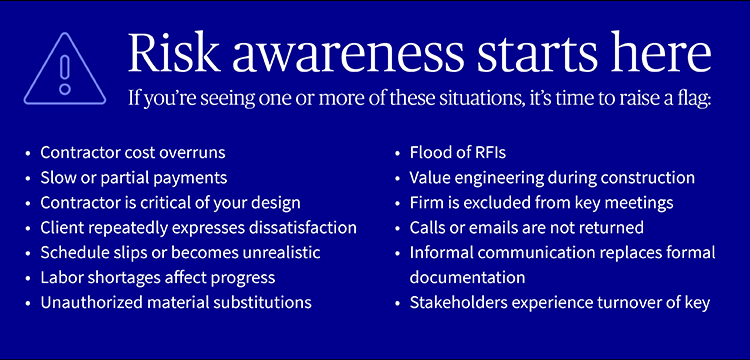

Recognizing the warning signs

Sometimes the people closest to risk can fail to spot the warning signs. That’s why risk awareness training is so important.

Staff may not realize they’re seeing the early stages of a claim. Reinforcing pattern recognition—and giving team members permission to act—is critical. When staff recognize these patterns and know it’s okay to speak up, they can prevent problems before they escalate.

Building a risk awareness culture

Avoiding claims isn’t just about contracts and quality control. It requires a firm-wide culture where everyone understands their role in managing risk. Risk management should be part of employee onboarding and regularly reinforced. Staff should understand your insurance coverage—what’s included, what’s excluded, and which costs (like redesign time) are not reimbursed. Most importantly, they should know when and how to escalate a concern—and trust that they’ll be supported when they do. Situational awareness only helps if there’s a clear path for raising the issue. You can’t just say “speak up”—you have to back that up with process and culture.

Putting risk awareness into practice

Here are some ways to embed risk awareness into your firm’s everyday operations:

- Include risk training in new employee onboarding and make sure all staff in your firm understand the policy benefits of AXA XL’s loss prevention assistance and early circumstance reporting.

- Hold quarterly “lessons learned” sessions.

- Establish a clear, non-punitive process for raising concerns.

- Recognize and reward staff who identify potential problems early.

- Make sure staff has a general understanding of how your PL insurance works.

- Make risk awareness part of performance reviews and growth plans.

- Engage with your broker to learn more about AXA XL Design Professional’s library of claims case studies and other programs, like “Warning Signs of a Claim,” on our EDGE learning management system.

Claims aren’t just legal events—they’re also business risks

Embedding these practices gives your team the tools they need—but mindset matters, too.

A single claim can wipe out profits from months of work, distract leadership from high-value projects, and damage long-term client trust. But most claims don’t start with catastrophic failures—they start with early signals that go unrecognized or unaddressed.

When your team understands the business impact of a claim and that everyone has a stake in the firm’s success, they become your strongest risk management tool.

By fostering risk literacy and situational awareness, you build a smarter, more resilient firm—one that can navigate complexity, protect its interests, and respond early when something doesn’t seem right.

1. To calculate the gross revenue needed to recover a deductible:

Dollar amount of deductible ÷ firm’s profit margin = required additional revenue

For example: $25,000 deductible ÷

• 5% profit margin = $500,000 additional revenue needed

• 10% profit margin = $250,000 additional revenue needed

• 15% profit margin = $166,667 additional revenue needed